The Real Barrier to Starting Therapy Most People Don’t Expect

You have at last made up your mind to do it.

It was not as quick as it ought to have been. Months of promising yourself that you would look into it, weeks of nearly dialing the phone, a few evenings of just sitting there looking at an open browser window that you could just open and close without a read. You’re here now, though. You are ready. You have done the hardest thing, which is deciding.

So you call your insurance company.

The hold music starts. Something vaguely classical, compressed to tinny meaninglessness by a phone line that sounds like it was installed in 1994. An automated voice tells you your call is very important. It informs you that the approximated wait time is twelve minutes. Then after fourteen minutes, someone picks up and requests your membership ID, date of birth, address, and the purpose of your call, and directs you to another department. The hold music starts again. Different song. Same feeling.

Twenty-three minutes later, you have a partial answer to a question you were not quite sure how to ask. Three new questions that you did not have when you started. And a vague, particular exhaustion, which has nothing to do with the original problem and everything to do with the system you just tried to navigate while carrying it.

This is what no one speaks about when they discuss those barriers to mental health treatment.

Not the stigma, not the courage it takes to ask for help. What doesn’t get discussed enough is this: the moment you finally gather the nerve to reach out is also the moment the American insurance system hands you the most confusing paperwork of your life and wishes you luck.

This article is about cutting through that.

Understanding “In-Network” Coverage

In-network means the provider. The clinic, the program, and the therapist have a contract with your insurance company. They’ve agreed on rates in advance. Therefore, when seeking the services of an in-network provider, your insurer will cover a certain amount of the price, and you will only have to cover your deductible, copayment, or coinsurance, depending on your particular plan.

Out-of-network indicates the absence of a contract. The provider charges their standard rate. Your insurer may cover a portion, a smaller portion, or none at all, depending on your plan. And you are responsible for the difference.

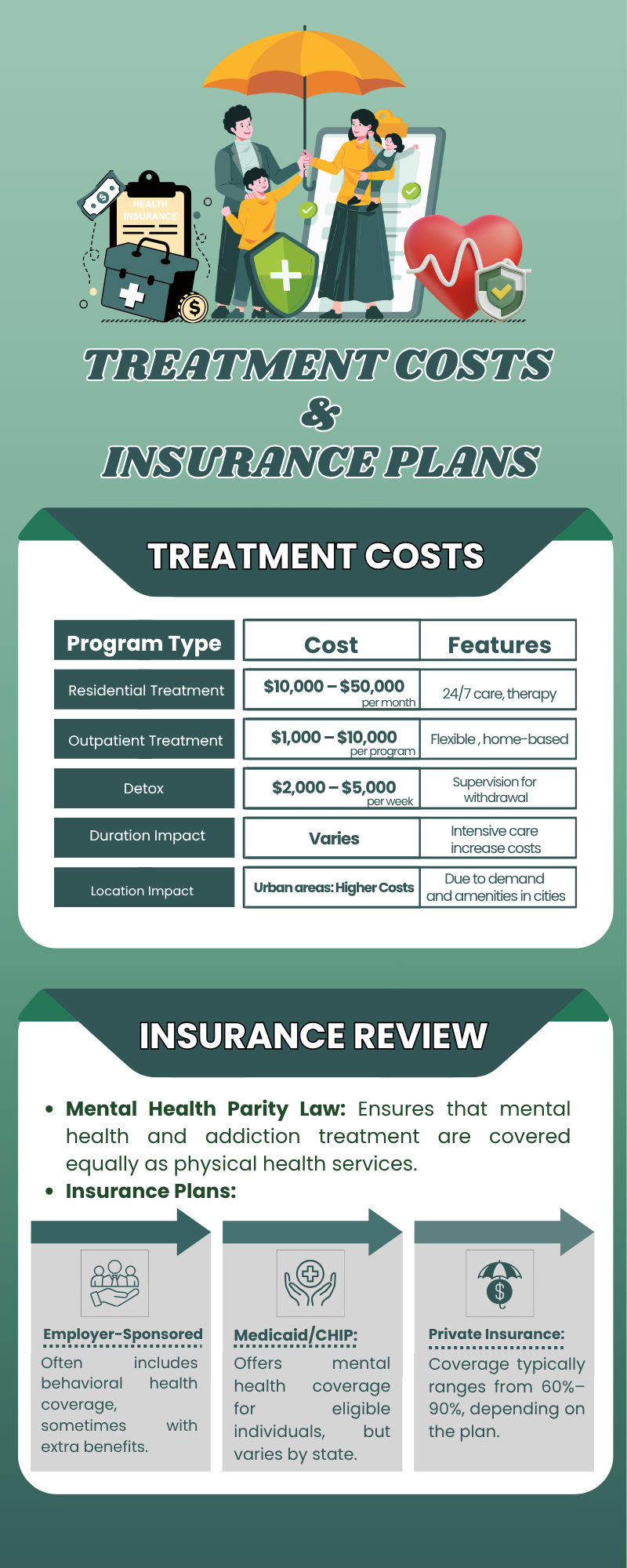

For Intensive Outpatient Programs, this difference is not marginal. Out-of-pocket IOP costs without in-network coverage can run anywhere from $3,000 to $10,000 for a single treatment episode. With in-network coverage, your out-of-pocket responsibility typically drops to whatever you owe toward your deductible and a copay per session. Often, a fraction of the total cost. For many people, in-network coverage is the difference between treatment being something they can actually do and treatment being something they read about and set aside.

The word in-network is not a technicality. It is the difference between a door that opens and one that doesn’t.

The Mental Health Parity Law

Most people have never heard of the Mental Health Parity and Addiction Equity Act. Most people who have heard of it don’t know what it guarantees. This is worth knowing before you talk to your insurance company, because it changes the conversation you’re allowed to have.

Federal law requires that insurers offering mental health coverage must provide it at parity with physical health coverage. This means the limitations they apply to mental health treatment – like visit caps, prior authorization requirements, and coverage restrictions – cannot be more restrictive than the limitations they apply to comparable medical or surgical treatment. IOP is explicitly included. If your plan covers intensive outpatient care for a physical condition, it must cover intensive outpatient care for a mental health condition at the same level.

Insurers do not always lead with this information. Some denials are legitimate. Some are not, and they get accepted because the person on the other end of the phone doesn’t know they have the right to push back. Knowing the law exists means knowing when a denial deserves an appeal and that appeals, filed correctly, succeed more often than most people realize.

What Insurance Covers in IOP And What to Ask

The vast majority of the big insurers, such as Aetna, Blue Cross Blue Shield, Cigna, United Healthcare, and Humana, cover Intensive Outpatient Programs, provided there is a medical necessity. Medically necessary, in practice, means a clinician has determined that your symptoms and level of functioning require this level of care. A proper intake assessment establishes this.

Before you enroll in any program, there are specific questions worth asking your insurer directly. Does my plan cover IOP for mental health? What is my deductible, and how much of it have I met? What is my copay or coinsurance per session? Is prior authorization required, and if so, who handles that? What is my out-of-pocket maximum for the year?

These questions have answers. The answers are in your plan documents and accessible by phone. Getting them before you enroll means no surprises on a bill that arrives six weeks after treatment ends.

What In-Network IOP at Clover Looks Like

At Clover Behavioral Health in Salem, NH, we work with most major insurance plans and handle verification on your behalf from the first conversation. You don’t need to arrive with the insurance piece figured out. You need to arrive. The rest is something we navigate together.

The intake process begins with a real clinical conversation. Not a form, not a checklist, but an honest discussion about where you are and what level of care makes sense for your situation. If IOP is the right fit, we confirm your coverage, clarify your out-of-pocket costs, and handle prior authorization so the administrative weight doesn’t land on you at the moment you least need it.

The program itself is the same quality of clinical care regardless of what your insurance looks like. Evidence-based treatment, licensed clinicians, and a structure built around your actual life. The in-network piece means that care is financially accessible. That the door opens at a cost that doesn’t require you to choose between treatment and the rest of your life.

Reach out today or call 978-216-7765. Bring your insurance card and your questions. Leave the hold music behind.

You made the hard decision. Let us handle the paperwork!