How Some IOP Programs Help Patients Navigate Insurance Approvals

Prior authorization, medical necessity reviews, and appeals are common in mental health coverage. This guide explains how the system works.

There is a card in your wallet with an insurance company’s name on it.

You’ve paid for it every month for years. Quietly, automatically, the way you pay for things you hope you’ll never need. It has always been there, in the slot behind your driver’s license, representing something you understood as a promise. You pay. They cover. That is the agreement. That is what the card means.

Now you need it. And the card, it turns out, is not a door. It is the beginning of a conversation with a system that was not designed around your convenience, your timeline, or your moment of readiness. The card is real. The coverage is real. Nonetheless, between the card and the care sits a machinery of prior authorizations, medical necessity determinations, utilization reviews, and appeals processes that most people encounter for the first time at exactly the moment they are least equipped to navigate them.

This is not an accident. It is architecture.

What follows is what that architecture looks like and how a program that knows it well makes sure it doesn’t stop you from getting better.

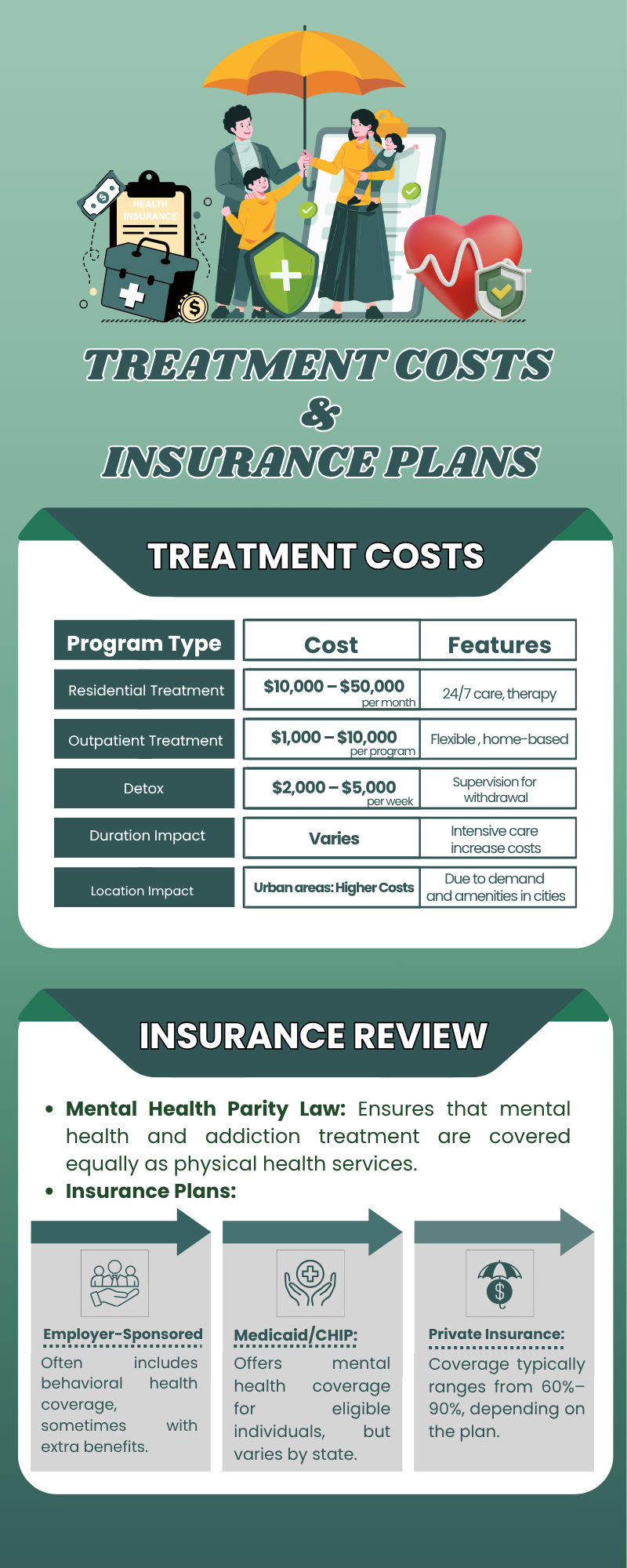

What Commercial Insurance Does And Doesn’t Guarantee

Having commercial insurance that covers mental health treatment does not mean IOP is automatically approved. This is the first thing most people discover too late, mid-process, when the friction has already cost them the momentum they couldn’t afford to lose.

Commercial insurers cover IOP. They are required to under federal law, but coverage and approval are two different things. Before treatment begins, most commercial plans require prior authorization: a formal determination by the insurer that your treatment is medically necessary. This determination is made not by your clinician, not by someone who has met you, but by a reviewer at the insurance company working from criteria you have never seen and were never given the opportunity to address.

Denials happen. They happen more than insurers publicly acknowledge. What most people don’t know and what changes everything once they do is that appealed denials succeed between 39 and 59 percent of the time, depending on the insurer and the state.

Insurers count on the fact that fewer than one percent of people ever file an appeal. The system is not unbeatable. It is counting on your exhaustion.

The Prior Authorization Playbook: What Insurers Are Really Doing

Most denials are not random. They follow a script, and knowing the script is the first step toward responding to it effectively.

The most common denial is a medical necessity determination. A claim that you are stable enough for standard outpatient therapy and do not require the intensity of IOP. This determination is often made on the basis of a brief clinical summary, without the full context of your history, your environment, or the specific ways that weekly therapy has already proven insufficient. It sounds clinical. It is frequently a first-pass decision designed to be reversed on appeal when documentation is provided.

The second common script is step therapy. A requirement that you demonstrate you have already tried and failed at a lower level of care before IOP will be approved. For people who have been in weekly therapy for months or years without adequate progress, this requirement is easy to satisfy. It just requires someone who knows how to document it correctly.

The third is frequency and session limits, caps on how many sessions are covered per week or per episode of care. Under the Mental Health Parity and Addiction Equity Act, these caps cannot be more restrictive than the limits applied to comparable physical health treatment. If your plan covers intensive cardiac rehabilitation three times a week without a session cap, it cannot legally apply stricter criteria to mental health IOP. Most people never know to make this argument. It is an argument worth making.

The Federal Law That Works in Your Favor

The Mental Health Parity and Addiction Equity Act is not new, as it has been in existence since 2008. The majority of those who would need it are not even aware of it.

What it guarantees, simply put: insurers may not impose stricter prior authorization conditions, treatment restrictions, and coverage conditions on mental health and substance use treatment compared to similar medical and surgical treatment. IOP is explicitly included.

The Consolidated Appropriations Act of 2021 added teeth to this guarantee, requiring insurers to conduct and document comparative analyses proving their mental health coverage criteria are no more restrictive than their medical coverage criteria. These analyses are available to you upon request. Requesting one, or having your treatment provider request one on your behalf, signals to the insurer that the person they are dealing with knows the rules of the game.

This is not litigation. It is leverage. The kind that exists specifically because Congress recognized that insurers were systematically applying stricter standards to mental health treatment and decided that needed to stop. The law is on your side. Using it requires knowing it exists.

What “Accepts Commercial Insurance” Means at Clover

There is a meaningful difference between a program that accepts commercial insurance and a program that actively navigates it on your behalf. The first means your insurer is on their list. The second means you don’t have to fight your own insurance company while simultaneously trying to get better.

At Clover Behavioral Health in Salem, NH, insurance verification begins before your first session. Not as a formality, but as a complete picture of your coverage. What your plan covers. What your deductible is and how much of it remains. What your copay or coinsurance per session will be. Whether prior authorization is required and what documentation it needs. All of this gets handled by people who do it every day, who know the specific language each major carrier responds to, and who understand that a prior authorization filed correctly the first time is faster and less exhausting than one filed incorrectly and appealed.

The major commercial carriers accepted at Clover include Aetna, Blue Cross Blue Shield, Cigna, United Healthcare, and Humana, among others. If your plan is not immediately familiar, the first conversation includes a real-time check instead of we’ll look into it.

Reach Out Clover Behavioral Health Today

Call us or reach out through our website. Bring your insurance card and your questions. We’ll tell you exactly what your plan covers, exactly what it will cost, and what happens next. No surprises. No waiting for approval while the moment passes.

The card works. Let us show you how.